Happy Holidays,

Did you know that there are actually economists who study theories about Christmas Presents. Greg Mankiw summarizes the research here.

The idea is that Christmas gifts are signalling mechanisms, because in theory giving money should be the optimal gift (since the person can spend the money on whatever he or she wants). However, if a gift is a signal to show how much you care about a person, giving money seems like a big cop out.

You can test this theory out on your boyfriend or girlfriend, give them a gift certificate and see how they like it. Next Christmas--if he or she is still around---you can give them a gift.

Sunday, December 24, 2006

Wednesday, December 20, 2006

Flat Panel Discounting

The price war for Flat Panel TV's is hitting high gear, with Circuit City being the hardest hit so far. Read more here

The price war has been a boon for consumers who, in some cases, were able to snap up the sets over the Thanksgiving weekend at below retailers' cost.

But growing competition and plummeting prices are taking a heavy toll on many retailers. The consumer-electronics market has turned into a free-for-all as the nation's largest electronics retailer, Best Buy Co., has fended off attacks by giant discounter Wal-Mart, which is looking to electronics to help recharge its growth. Flat-panel TVs this season also have cropped up for sale in such unaccustomed venues as home-improvement outlets, office-supply stores and discount chains.

This would be the classic example of a price war among Oligopolists

"Not only did the electronics chain withstand Wal-Mart's initial onslaught, it has continued to gain share. After Wal-Mart publicly crowed about its plan to offer a glitzy Panasonic plasma high-definition TV set for $1,294 the day after Thanksgiving, Best Buy fired back by offering the same TVs for $1,000 and calling it an "unadvertised special.""

The price war has been a boon for consumers who, in some cases, were able to snap up the sets over the Thanksgiving weekend at below retailers' cost.

But growing competition and plummeting prices are taking a heavy toll on many retailers. The consumer-electronics market has turned into a free-for-all as the nation's largest electronics retailer, Best Buy Co., has fended off attacks by giant discounter Wal-Mart, which is looking to electronics to help recharge its growth. Flat-panel TVs this season also have cropped up for sale in such unaccustomed venues as home-improvement outlets, office-supply stores and discount chains.

This would be the classic example of a price war among Oligopolists

"Not only did the electronics chain withstand Wal-Mart's initial onslaught, it has continued to gain share. After Wal-Mart publicly crowed about its plan to offer a glitzy Panasonic plasma high-definition TV set for $1,294 the day after Thanksgiving, Best Buy fired back by offering the same TVs for $1,000 and calling it an "unadvertised special.""

Tuesday, December 19, 2006

Sidebar

For some reason the sidebar has shifted to the bottom of the page. I don't know why. All the links are there, however, you just have to scroll to the bottom.

PS-If this fixes itself, please ignore

PS-If this fixes itself, please ignore

Monday, December 18, 2006

Market Assumptions

This is a recap of the review class and could serve as notes on what to keep in mind on the 4 market models. While 4 models may seem like a lot to memorize, try and think of everything as either flowing from or contradicting the assumptions of perfect competition.

Remember the 4 assumptions

1) Many buyers and sellers

2) Perfect information

3) Easy entry/exist

4) Homogenous product.

Monopolistic competition deviates from assumption 4.

Monopoly deviates from 1 and 3

and Oligopoly deviates from 1 and 3, though to a lesser extent (since there is more than one firm, and there is possible entry/exit). 4 is also likely violated, as in monopolistic competition (think the Video Console industry or Flat Panel TV's).

Remember the 4 assumptions

1) Many buyers and sellers

2) Perfect information

3) Easy entry/exist

4) Homogenous product.

Monopolistic competition deviates from assumption 4.

Monopoly deviates from 1 and 3

and Oligopoly deviates from 1 and 3, though to a lesser extent (since there is more than one firm, and there is possible entry/exit). 4 is also likely violated, as in monopolistic competition (think the Video Console industry or Flat Panel TV's).

Study Hints for Final Exam

If I were you, I would be focusing on allocative efficiency and productive efficiency.

It is key to keep in mind that only under perfect competition is allocative efficiency (P=MC) and productive efficiency {min(ATC)} easily achieved.

In other markets, since some form of market imperfection exists (differentiated products, barriers to entry, small number of sellers, whatever) price does not necessarily equal marginal cost and ATC is not necessarily minimized.

Whether the government needs to step in and fix the problem, however, is another question, since the problem may be very small and may yield external benefits (in the form of product differentiation.)

It is key to keep in mind that only under perfect competition is allocative efficiency (P=MC) and productive efficiency {min(ATC)} easily achieved.

In other markets, since some form of market imperfection exists (differentiated products, barriers to entry, small number of sellers, whatever) price does not necessarily equal marginal cost and ATC is not necessarily minimized.

Whether the government needs to step in and fix the problem, however, is another question, since the problem may be very small and may yield external benefits (in the form of product differentiation.)

Friday, December 15, 2006

Thursday, December 14, 2006

Ice Skating and the Invisible Hand

This post illustrates the invisible hand via Ice Skating. Think about it: No one plans the traffic flow on an ice skating rink, yet ice skating is not complete chaos.

Wednesday, December 13, 2006

College Tuition and the "Baumol effect"

Take a look at this post by Professor Mankiw. Note in particular point 2, which explains the Baumol effect. The Baumol effect explains why wages can rise in a particular industry even if productivity growth in that industry is not rising. What matters is overall productivity, which ends up bidding up wages in all industries.

Quiz 10 - Comparative Advantage (Part I)

Quiz 10 - Comparative Advantage (Part I) Part II is 5 questions in class, which will be given on Thurs. The final is Tues 19th

1) (5 points) Below is the maximum amount of CD's or PC's that can be built by the US and Japan.

Pre-Specialisation

UK

Personal Computers

2,000

CD Players

500

Japan

Personal Computers

4,000

CD Players

2,000

1) Who has the absolute advantage in PC's?

2) Who has the absolute advantage in CD players?

3) Who has the comparative advantage in PC's?

4) Who has the comparative advantage in CD Players?

5) Based on this, who should specialize in CD Players and who should specialize in PC's?

6) Name and explain 2 objections to free trade and the counter argument provided by Economists.

1) (5 points) Below is the maximum amount of CD's or PC's that can be built by the US and Japan.

Pre-Specialisation

UK

Personal Computers

2,000

CD Players

500

Japan

Personal Computers

4,000

CD Players

2,000

1) Who has the absolute advantage in PC's?

2) Who has the absolute advantage in CD players?

3) Who has the comparative advantage in PC's?

4) Who has the comparative advantage in CD Players?

5) Based on this, who should specialize in CD Players and who should specialize in PC's?

6) Name and explain 2 objections to free trade and the counter argument provided by Economists.

Monday, December 11, 2006

Game Theory Application

This is a good application of game theory. Ever wonder why ATM fees persist in a brutally competitive banking industry? Or why hotels charge you $2 for a local phone call and $5 for a coke at the mini bar?

Friday, December 08, 2006

Various articles on Free Trade

Here is New York Times Columnist Nicholas D. Kristof on Sweatshops

Here is an article in the New Republic criticizing the Schumber/Roberts attack on free trade. The first few paragraphs give a good summary of what trade does to boost production. (Note: I would link to Schumer's original article but it is not available free online). But here is another blogger being less kind to Schumer on this issue.

If this is all confusing to you, let me try and explain comparative advantage using the following example. Let us assume there is a doctor and a secretary. The doctor has an absolute advantage in both surgeries and typing (he is the fastest typist in the world). In autarky (i.e. the position of no trade) he does a good number of surgeries but also a lot of time consuming typing. The secretary is unemployment or working at a lower wage job.

Comparative advantage says that it is advantagous for the Doctor to hire the Secretary to do his typing for him. This way he can concentrate on surgeries (boost his output on surgeries, where he makes a lot of money) and leave the typing to the secretary. It does not matter that the Secretary is a slower typist than he is. What matters is that by hiring the Secretary, he leaves more room to specialize in a field he can make a lot of money in and boost overall output. The Secretary is also better off because she is at a nice job with the Doctor whereas before she was either unemployment or working for much less money.

E-mail me if you are still having trouble.

Here is an article in the New Republic criticizing the Schumber/Roberts attack on free trade. The first few paragraphs give a good summary of what trade does to boost production. (Note: I would link to Schumer's original article but it is not available free online). But here is another blogger being less kind to Schumer on this issue.

If this is all confusing to you, let me try and explain comparative advantage using the following example. Let us assume there is a doctor and a secretary. The doctor has an absolute advantage in both surgeries and typing (he is the fastest typist in the world). In autarky (i.e. the position of no trade) he does a good number of surgeries but also a lot of time consuming typing. The secretary is unemployment or working at a lower wage job.

Comparative advantage says that it is advantagous for the Doctor to hire the Secretary to do his typing for him. This way he can concentrate on surgeries (boost his output on surgeries, where he makes a lot of money) and leave the typing to the secretary. It does not matter that the Secretary is a slower typist than he is. What matters is that by hiring the Secretary, he leaves more room to specialize in a field he can make a lot of money in and boost overall output. The Secretary is also better off because she is at a nice job with the Doctor whereas before she was either unemployment or working for much less money.

E-mail me if you are still having trouble.

Thursday, December 07, 2006

Video Game Price Wars

Here is the Wikipedia article on the price wars in the Video Game industry. This is a good example of an Oligopoly price war at work.

There are a number of reasons why this price war took place, but here is one of the more interesting reasons:

A flood of consoles on the market giving consumers too many choices. At the time of the U.S. crash, there was a plethora of consoles on the market: Atari 2600, Atari 5200, Bally Astrocade, Colecovision, Coleco Gemini, Emerson Arcadia 2001, Fairchild Channel F System II, Magnavox Odyssey2, Mattel Intellivision (and its just released update with slew of peripherals, Intellivision II), Sears Tele-Games systems (which included 2600 and Intellivision clones), Tandyvision, and Vectrex. Each one of these had their own library of games, and many had (in some cases large) 3rd party libraries. Likewise, many of these same companies announced yet another generation of consoles for 1984, such as the Odyssey3, and Atari 7800.[1]

There are a number of reasons why this price war took place, but here is one of the more interesting reasons:

A flood of consoles on the market giving consumers too many choices. At the time of the U.S. crash, there was a plethora of consoles on the market: Atari 2600, Atari 5200, Bally Astrocade, Colecovision, Coleco Gemini, Emerson Arcadia 2001, Fairchild Channel F System II, Magnavox Odyssey2, Mattel Intellivision (and its just released update with slew of peripherals, Intellivision II), Sears Tele-Games systems (which included 2600 and Intellivision clones), Tandyvision, and Vectrex. Each one of these had their own library of games, and many had (in some cases large) 3rd party libraries. Likewise, many of these same companies announced yet another generation of consoles for 1984, such as the Odyssey3, and Atari 7800.[1]

Wednesday, December 06, 2006

Video game market redux

This New Yorker piece on Nintendo vs placated 3 is quite interesting. Here is an interesting fact:

"Nintendo, though, has not just survived out of the spotlight; it has thrived. It has five billion dollars in the bank from years of solid profits, and this past year, though it spent heavily on the launch of the Wii, it made close to a billion dollars in profit and saw its stock price rise by sixty-five per cent. Sony's game division, by contrast, barely eked out a profit and Microsoft reportedly lost money. Who knew bringing up the rear could be so lucrative?"

There seem to be a few explanations for this

1) Because Nintendo is not trying to dominate the market, they are making money on its consoles rather than losing $240 dollars a sale. This makes profits, at least in the short term, easier to come by

2) Nintendo makes more of its games in house rather than through 3rd parties. Therefore, the return on its investment is higher

3) You do not need to dominate the market in order to be successful. Although the Video Game industry (at least console wise) is an oligopoly, Nintendo can still thrive despite not being thdominantnt factor because it caters to a niche market that Playstation and X-Box are not capturing. And you don't need to develop a computer suited for high tech weaponry in order to satisfy them.

Of course, this doesn't mean that Sony will not dominate in the long run. The playstation 2 accounted for over half of Sony's profits just recently. All that is being inferred here is that Nintendo can still compete despite not having the dominant system.

"Nintendo, though, has not just survived out of the spotlight; it has thrived. It has five billion dollars in the bank from years of solid profits, and this past year, though it spent heavily on the launch of the Wii, it made close to a billion dollars in profit and saw its stock price rise by sixty-five per cent. Sony's game division, by contrast, barely eked out a profit and Microsoft reportedly lost money. Who knew bringing up the rear could be so lucrative?"

There seem to be a few explanations for this

1) Because Nintendo is not trying to dominate the market, they are making money on its consoles rather than losing $240 dollars a sale. This makes profits, at least in the short term, easier to come by

2) Nintendo makes more of its games in house rather than through 3rd parties. Therefore, the return on its investment is higher

3) You do not need to dominate the market in order to be successful. Although the Video Game industry (at least console wise) is an oligopoly, Nintendo can still thrive despite not being thdominantnt factor because it caters to a niche market that Playstation and X-Box are not capturing. And you don't need to develop a computer suited for high tech weaponry in order to satisfy them.

Of course, this doesn't mean that Sony will not dominate in the long run. The playstation 2 accounted for over half of Sony's profits just recently. All that is being inferred here is that Nintendo can still compete despite not having the dominant system.

Tuesday, December 05, 2006

Taco Bell

In a monopolistically competitive market, what do you think this news would do?

The fast food industry has differentiated products. Taco Bell fills a nitch for Latam fast food. But will it serve the Latam ecoli fast food market?

The fast food industry has differentiated products. Taco Bell fills a nitch for Latam fast food. But will it serve the Latam ecoli fast food market?

Monday, December 04, 2006

Quiz 9 due Tuesday Dec 5th

Quiz 9 – Intro to Micro Economics.

Professor Matthew Festa

Due in Class Tuesday Dec 05

1) State the 4 assumptions of perfect competition and then state the assumption(s) that monopolistic competition breaks. State the assumption(s) that an oligopoly breaks (2 points)

2) What is allocative efficiency? What is productive efficiency? Why does monopolistic competition fail to meet both of these? (2 points)

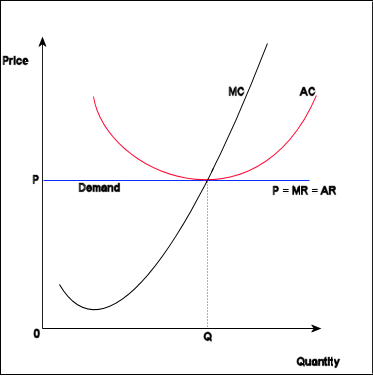

3) Explain why on the above graph, the demand curve slopes down for a monopolistically competitive firm. (2 points).

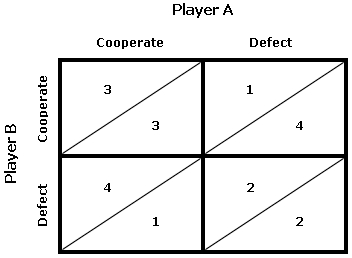

4) On the below table, explain which box would be the best case scenario for These two companies. What is Nash equilibrium? Explain why that is the point the market will tend towards. Think of Company A as Coca Cola and Company B as Pepsi. The numbers are profits for both companies in billions (so 3 = $3bn). (3 points).

{kind=link}

Sunday, December 03, 2006

Quiz 9

I will be posting the next quiz online tommorrow morning. You can turn it in either Tues or Thurs for no penalty.

Friday, December 01, 2006

How good is Jim Cramer's investment advise?

Jim Cramer is the eccentric CNBC analyst who gives stock picks at 6pm Mon-Fri (in a fairly wild manner). He was a former Hedge Fund Manager. How good is his investment advice against, say, a wild monkey. Click here for the surprising results.

There is actually theoretical backing for this and its called the efficient market hypothesis. The idea is related to perfect competition. Since there are so many buyers and sellers in the market that possess all necessary information about an investment (stocks, bonds etc) a professional money manager should not be able to outperform a normal buy and hold pattern of a well diversified portfolio. The evidence for this is actually quite strong.

The real kicker is what exactly do we mean by all information? Are we talking about all past price moves (the weak form), all publically available knowledge, including my predictions (the semi-strong) or all public and private knowledge (the strong form).

I think most economists would agree that most markets are either weak to semi-strong efficient markets. However, it looks like the market to predict the currenct Pope was strong form

There is actually theoretical backing for this and its called the efficient market hypothesis. The idea is related to perfect competition. Since there are so many buyers and sellers in the market that possess all necessary information about an investment (stocks, bonds etc) a professional money manager should not be able to outperform a normal buy and hold pattern of a well diversified portfolio. The evidence for this is actually quite strong.

The real kicker is what exactly do we mean by all information? Are we talking about all past price moves (the weak form), all publically available knowledge, including my predictions (the semi-strong) or all public and private knowledge (the strong form).

I think most economists would agree that most markets are either weak to semi-strong efficient markets. However, it looks like the market to predict the currenct Pope was strong form

Free Trade

Arnold Kling has a good introduction to a topic that we will be discussing shortly, free trade.

The main points of his article can be summarized by this story:

"The surgeon talks about needing to give her house a new coat of paint. Her tennis partner suggests that compared with a typical house painter she probably could do this job better herself. "That's true," the surgeon replies. "I have steady hands, and I work more carefully and efficiently than most painters. But I figured that even though it will take the painters 50 hours to do the house and I could do it in 40, it's still a better use of my time to see patients. I can pay the painters with the money I get from seeing patients for two hours, so in a way I can paint my house in just two hours by sticking to medicine."

This one:

Finally, the tennis partner says. "My brother-in-law had a kidney stone. I was going to recommend that he come to you, but his doctor said that there is a new pill that dissolves some stones. So he doesn't need surgery."

And finally, this comment:

"The last anecdote illustrates one of the most subtle benefits from trade. Competition and trade lead to innovation, in this case the development of a drug that reduces the cost and risk of removing kidney stones.

Competition and innovation are not necessarily a benefit for the surgeon. The demand for her services falls to the extent that medication can be used in place of surgery"

Me: Think about this another way. Free trade and technological innovation have destroyed numerous jobs in agriculture over the past century (before the 20th century America had many more jobs in agriculture. I believe the figure is now down to 2%.) But the gains from trade, an exponential increase in food production, vastly outweighed the loss of jobs in that industry. Further, with jobs opening up in industries that American had a comparative advantage in, people migrated towards those new jobs and normal economic development created other jobs. At the end of the day the economy has many more jobs now (at higher pay!) than they did 100 years ago.

The main points of his article can be summarized by this story:

"The surgeon talks about needing to give her house a new coat of paint. Her tennis partner suggests that compared with a typical house painter she probably could do this job better herself. "That's true," the surgeon replies. "I have steady hands, and I work more carefully and efficiently than most painters. But I figured that even though it will take the painters 50 hours to do the house and I could do it in 40, it's still a better use of my time to see patients. I can pay the painters with the money I get from seeing patients for two hours, so in a way I can paint my house in just two hours by sticking to medicine."

This one:

Finally, the tennis partner says. "My brother-in-law had a kidney stone. I was going to recommend that he come to you, but his doctor said that there is a new pill that dissolves some stones. So he doesn't need surgery."

And finally, this comment:

"The last anecdote illustrates one of the most subtle benefits from trade. Competition and trade lead to innovation, in this case the development of a drug that reduces the cost and risk of removing kidney stones.

Competition and innovation are not necessarily a benefit for the surgeon. The demand for her services falls to the extent that medication can be used in place of surgery"

Me: Think about this another way. Free trade and technological innovation have destroyed numerous jobs in agriculture over the past century (before the 20th century America had many more jobs in agriculture. I believe the figure is now down to 2%.) But the gains from trade, an exponential increase in food production, vastly outweighed the loss of jobs in that industry. Further, with jobs opening up in industries that American had a comparative advantage in, people migrated towards those new jobs and normal economic development created other jobs. At the end of the day the economy has many more jobs now (at higher pay!) than they did 100 years ago.

Thursday, November 30, 2006

Nassau County Stats

If you want to check out some interesting stastistics on our county, click here . Here is a hightlight with some thoughts by me below.

Nassau had the nation’s sixth-highest

median household income in 2004 ($78,762),

in part because many residents commute to

New York City for high-paying jobs.

• Personal income was the second-highest in

the State and represented almost 10 percent

of total New York State personal income.

• Nassau’s economy added jobs between 2003

and 2005, but at a slower pace than

surrounding areas. In 2005, total

employment averaged nearly 595,000 jobs.

• The sectors of trade, transportation and

utilities; education and health services; and

professional and business services account

for over half the jobs in Nassau.

• Nassau’s unemployment rate in the first

eight months of 2006 averaged 4 percent,

well below the State’s rate of 4.8 percent.

• In 2005, Nassau County’s average salary of

$46,010 was the third-highest in the State.

Average salaries in Nassau increased by

7.5 percent between 2003 and 2005.

The problem as I see it is that we do not have population growth. On the front page they say

"The population has remained stable, even

though the birth rate exceeds the death rate,

because more people are moving out of

Nassau than are moving in."

Since the costs of services ( police and education for example) are growing but our population is not, taxes have been heading up. With wages rising at a lower pace in the county than out, this presents a problem. While it looks like Demographics have played the major role (elderly moving to Florida), there is also the interesting emigration to Suffolk because Suffolk is further away from NYC than Nassau is.

Nassau had the nation’s sixth-highest

median household income in 2004 ($78,762),

in part because many residents commute to

New York City for high-paying jobs.

• Personal income was the second-highest in

the State and represented almost 10 percent

of total New York State personal income.

• Nassau’s economy added jobs between 2003

and 2005, but at a slower pace than

surrounding areas. In 2005, total

employment averaged nearly 595,000 jobs.

• The sectors of trade, transportation and

utilities; education and health services; and

professional and business services account

for over half the jobs in Nassau.

• Nassau’s unemployment rate in the first

eight months of 2006 averaged 4 percent,

well below the State’s rate of 4.8 percent.

• In 2005, Nassau County’s average salary of

$46,010 was the third-highest in the State.

Average salaries in Nassau increased by

7.5 percent between 2003 and 2005.

The problem as I see it is that we do not have population growth. On the front page they say

"The population has remained stable, even

though the birth rate exceeds the death rate,

because more people are moving out of

Nassau than are moving in."

Since the costs of services ( police and education for example) are growing but our population is not, taxes have been heading up. With wages rising at a lower pace in the county than out, this presents a problem. While it looks like Demographics have played the major role (elderly moving to Florida), there is also the interesting emigration to Suffolk because Suffolk is further away from NYC than Nassau is.

The Mineola Police Issue Part II

The debate over whether Mineola should form its own police force has gotten interesting. As I see it, the main complaint seems to be that taxes will go up and we don't know what we will be betting in return. As to the former issue, I have already spoken, but with regards to whether we are opening up a Pandora's box, I just don't see the complaint.

First, as this article demonstrates, about 25 villages nationwide have adopted community police departments and they seem to be satisfied with them. Further, Long Island already has a number of Village Police Departments--Garden City and Floral Park for example---and they seem satisfied with them. To put it another way, there has been no movement towards joining the county but there has been movement towards establishing separate community police departments. That is telling, in my opinion.

How does this relate to what we are learning in class? It goes back to the issue of costs and benefits. Taxes are going up county wide for the Police Department at the same time Police service is being cut. By separating the community policing aspect from the County, Mineola has a chance at increasing coverage at the same (or possibly less) cost.

Another way this relates to our class has to do with specialization. While we talked about specialization in terms of increasing size (and specializing in specific features such as produing the head of pin instead of the entire pin), the theory is related to the Village Police Department. By specializing in Mineola Police issues, the Officers will have specialized knowledge of the Village, its needs and its hot spots.

First, as this article demonstrates, about 25 villages nationwide have adopted community police departments and they seem to be satisfied with them. Further, Long Island already has a number of Village Police Departments--Garden City and Floral Park for example---and they seem satisfied with them. To put it another way, there has been no movement towards joining the county but there has been movement towards establishing separate community police departments. That is telling, in my opinion.

How does this relate to what we are learning in class? It goes back to the issue of costs and benefits. Taxes are going up county wide for the Police Department at the same time Police service is being cut. By separating the community policing aspect from the County, Mineola has a chance at increasing coverage at the same (or possibly less) cost.

Another way this relates to our class has to do with specialization. While we talked about specialization in terms of increasing size (and specializing in specific features such as produing the head of pin instead of the entire pin), the theory is related to the Village Police Department. By specializing in Mineola Police issues, the Officers will have specialized knowledge of the Village, its needs and its hot spots.

Great article on Milton Friedman

Brad Delong, a respected liberal economist, has written an intelligent piece on the legacy of Milton Friedman here.

His main contention, that Friedman completed and corrected Keynes, seems right to me.

His main contention, that Friedman completed and corrected Keynes, seems right to me.

Tyler Cowen on Immigration

Economist Tyler Cowen has an interesting article in the New York Times today on immigration. He bring up an interesting issue with current immigration. Although the benefits outweigh the costs, it can be made better (and more acceptable) if we decrease the education gap.

"A high school diploma brings higher wages in Mexico, but in the United States the more educated migrants do not earn noticeably more than those who have less education. Education does not much raise the productivity of hard physical labor. The result is that the least educated Mexicans have the most reason to cross the border. In addition, many Mexicans, knowing they may someday go to the United States, see less reason to invest in education"

One solution he offers is to combine tighter border security with an increase in legal immigration , and require more education.

"A high school diploma brings higher wages in Mexico, but in the United States the more educated migrants do not earn noticeably more than those who have less education. Education does not much raise the productivity of hard physical labor. The result is that the least educated Mexicans have the most reason to cross the border. In addition, many Mexicans, knowing they may someday go to the United States, see less reason to invest in education"

One solution he offers is to combine tighter border security with an increase in legal immigration , and require more education.

What Economists Believe

Greg Mankiw and Arnold Kling post survey results of Economist opinions. There is actually a wide range of agreeement on many key issues.

Here is a sample:

87.5 percent agree that "the U.S. should eliminate remaining tariffs and other barriers to trade."

85.2 percent agree that "the U.S. should eliminate agricultural subsidies."

85.3 percent agree that "the gap between Social Security funds and expenditures will become unsustainably large within the next fifty years if current policies remain unchanged."

77.2 percent agree that "the best way to deal with Social Security's long-term funding gap is to increase the normal retirement age."

67.1 percent agree that "parents should be given educational vouchers which can be used at government-run or privately-run schools."

65.0 percent agree that "the U.S. should increase energy taxes

From what you learned in class, what do you think is behind these beliefs?

Here is a sample:

87.5 percent agree that "the U.S. should eliminate remaining tariffs and other barriers to trade."

85.2 percent agree that "the U.S. should eliminate agricultural subsidies."

85.3 percent agree that "the gap between Social Security funds and expenditures will become unsustainably large within the next fifty years if current policies remain unchanged."

77.2 percent agree that "the best way to deal with Social Security's long-term funding gap is to increase the normal retirement age."

67.1 percent agree that "parents should be given educational vouchers which can be used at government-run or privately-run schools."

65.0 percent agree that "the U.S. should increase energy taxes

From what you learned in class, what do you think is behind these beliefs?

Wednesday, November 29, 2006

Presidential Candidates picking economic advisors

2008 Republican presidential candidates have started to pick their congressional candidates. Looks like they are starting early.

Nintento vs PlayStation

The WSJ has a good article comparing the new Nintendo to the new Playstation system. You can read it here

The description of the two clearly shows that we have a heterogeneous product and we are no longer in "perfect competition," but rather "monopolistic competition."

"The PS3 includes a hard disk, a networking port, Wi-Fi wireless networking, and playback of DVDs and CDs. It produces high-definition video. In fact, the PS3 can also play a next-generation, high-definition movie disk, called Blu-ray...The Wii is a small, thin white box that costs just $250 and has much wimpier specs than the Sony. It does have Wi-Fi, but it lacks a hard disk, a networking port, and the ability to play DVDs or CDs, let alone Blu-ray disks. It cannot produce high-definition video. It has fewer ports and connectors."

It is also clear that the two machines are targeting two different types of "gamers"

"The Wii is for casual game players, including younger kids and older adults who find the complexity and finger skills required for the PlayStation and Xbox to be intimidating. Even adventure games and racing games on the Wii seem easier to get into than similar titles on the PS3."

Tuesday, November 28, 2006

Bernanke on the Economy

Fed Chairman Bernanke speaks on the economy here .

On GDP growth (Economic Growth)

"the pace of economic activity has moderated over the course of the year. According to the latest estimates by the U.S. Department of Commerce, real gross domestic product (GDP) increased at an annual rate of 2.6 percent in the second quarter of 2006 and at a rate of only 1.6 percent in the third quarter. These figures are down noticeably from the 3-1/2 percent average pace of growth of the preceding two years. We will receive an updated estimate of third-quarter GDP growth tomorrow. At this juncture, information about economic activity in the fourth quarter is limited, and the range of plausible outcomes remains wide. But the indicators in hand suggest that real GDP growth this quarter is likely to be in the same general range that it was in the second and third quarters"

On Inflation

" Core inflation is expected to slow gradually from its recent level, reflecting the reduced impetus from high prices of energy and other commodities, contained inflation expectations, and perhaps further reductions in the rate of increase of shelter costs and some easing in the pressures on capital and labor resources. However, substantial uncertainties surround this baseline forecast...In its latest statement, the FOMC reiterated its view that the upside risks to inflation are the predominant risks to the forecast and indicated that it is prepared to take action to address inflation if developments warrant. "

On the Housing Sector...cutting to the heart of the matter.

"Notwithstanding the sharp reduction in starts of new single-family houses, inventories of both new and existing homes for sale have increased markedly this year. For example, according to the most recent data, homebuilders currently have about 550,000 new homes for sale, roughly half again the number that has been typical during the past decade. Moreover, the official statistics likely understate the full extent of the inventory buildup, as many homebuilders have reported a sharp increase this year in the number of buyers canceling signed contracts. A home for which the sales contract is cancelled becomes available for sale once again but is not included in the official data on the inventory of unsold new homes. To reduce this inventory overhang, builders are likely to continue to limit the number of new homes under construction. "

Note: Remember your basic supply and demand. High prices combined combined with large inventories are a recipe for reductions in price and cuts in output. This is because high inventories mean surplus, so suppliers cut prices (leading to a decrease in quantity supplied) in order to induce more demanders in the market.

From a Macro point of view (if you want to learn more about this, sign up for my macro class) the direct risk from the housing sector is decreases in construction. This in itself is (probably) not enough to induce a recession unless it is combined with an indirect effect, which would come in the form of lower consumer spending. The tranmission here is that lower home prices reduce net wealth and decreaes the amount of cash someone could extract from their home to fund current consumption (in the form of home improvements, etc.). But we will see.

On GDP growth (Economic Growth)

"the pace of economic activity has moderated over the course of the year. According to the latest estimates by the U.S. Department of Commerce, real gross domestic product (GDP) increased at an annual rate of 2.6 percent in the second quarter of 2006 and at a rate of only 1.6 percent in the third quarter. These figures are down noticeably from the 3-1/2 percent average pace of growth of the preceding two years. We will receive an updated estimate of third-quarter GDP growth tomorrow. At this juncture, information about economic activity in the fourth quarter is limited, and the range of plausible outcomes remains wide. But the indicators in hand suggest that real GDP growth this quarter is likely to be in the same general range that it was in the second and third quarters"

On Inflation

" Core inflation is expected to slow gradually from its recent level, reflecting the reduced impetus from high prices of energy and other commodities, contained inflation expectations, and perhaps further reductions in the rate of increase of shelter costs and some easing in the pressures on capital and labor resources. However, substantial uncertainties surround this baseline forecast...In its latest statement, the FOMC reiterated its view that the upside risks to inflation are the predominant risks to the forecast and indicated that it is prepared to take action to address inflation if developments warrant. "

On the Housing Sector...cutting to the heart of the matter.

"Notwithstanding the sharp reduction in starts of new single-family houses, inventories of both new and existing homes for sale have increased markedly this year. For example, according to the most recent data, homebuilders currently have about 550,000 new homes for sale, roughly half again the number that has been typical during the past decade. Moreover, the official statistics likely understate the full extent of the inventory buildup, as many homebuilders have reported a sharp increase this year in the number of buyers canceling signed contracts. A home for which the sales contract is cancelled becomes available for sale once again but is not included in the official data on the inventory of unsold new homes. To reduce this inventory overhang, builders are likely to continue to limit the number of new homes under construction. "

Note: Remember your basic supply and demand. High prices combined combined with large inventories are a recipe for reductions in price and cuts in output. This is because high inventories mean surplus, so suppliers cut prices (leading to a decrease in quantity supplied) in order to induce more demanders in the market.

From a Macro point of view (if you want to learn more about this, sign up for my macro class) the direct risk from the housing sector is decreases in construction. This in itself is (probably) not enough to induce a recession unless it is combined with an indirect effect, which would come in the form of lower consumer spending. The tranmission here is that lower home prices reduce net wealth and decreaes the amount of cash someone could extract from their home to fund current consumption (in the form of home improvements, etc.). But we will see.

Department of Useless information

Did you know that you can survive in outerpace exposed for up to 2 minutes without suffering any long term problems? No?

Hat tip Tyler Cowen

Hat tip Tyler Cowen

Physics vs Economics?

This is an amusing post on why citizens often give absolute deference to Physicists but not to Economists.

Monopolistic Competition and Oligopoly

Mineola Police Force and Marginal Utility

Using Economics: The Mineola Police Force.

The Village of Mineola is considering opting out of the Nassau County Police Force and establishing its own police force (ala Garden City). To read a summary of the debate (scheduled for a vote on Dec 5th), click here. For a more detailed summary, click here

This is certainly a contentious issue, but how can we use economics to wade through the debate?

1) Rational Ignorance and vested interests - The first topic we can use is the idea of government failure. That is, most of the voters are rationally ignorant about how their taxes are being used. How many people here know how much of their property taxes went towards funding the Nassau County Police Department? On the other hand, the Police department has a strong vested interest in maintaining the revenue source coming from Mineola (estimated at $6.7mn dollars a year). Part of the problem seems to be that taxes have gone up while coverage has gone down. A first pass look at this suggests that the increase salaries of police officers over the years has made it harder to hire police officers (since that increases revenues and necessitates a tax hike. With taxes at already high levels in the county, this is a problem.)

On the other hand, the village certainly has a vested interest in making sure the report favors establishing a police department rather than maintaining the current service (although the Village debate mentioned this, they curiously understated the vested interest mentioned above). However, from the standpoint of the Village residents, a Village police force would bring the police closer to the "check" of the voters. That is, if the residents are unsatisfied with how things are going they can vote in a change. The mayor, in turn, has a vested interest in getting re-elected so he is unlikely to want things to spiral out of control. As far as I can tell, the voters do not have this choice under the current police force (since their votes are dispersed among the county).

2) Marginal Utility - However, the economics of government can only take us so far here. The key issue is whether the marginal utility per tax dollar goes up or go down. So the question for residents becomes, how much "juice" (police coverage) am I getting for the "squeeze" (tax dollars). But this makes the whole debate about a tax hike completely irrelevant. If the marginal utility of the tax dollars goes up, you should support it. If it goes down, you should oppose it. Here is how I can demonstrate this:

Assume that initially you pay $100 a year in taxes to the government for police protection (your coverage is the Nassau Police Force). Assume also that there is only one type of crime, robbery, and that crime, if committed, will cost you $100,000. Finally assume that the police force, via the deterrant of arrest and prosecution, lowers the risk of arrest to 1% (0.01). Without a police force the probability of your home being robbed is 25%

The benefit to you of the police force is, of course, huge. Without it the expected cost of a robbery is $25,000. With a police force it is $1000. (According to Marginal Utility theory you should support a measure so long as the MB>MC. Here the Marginal Cost is $200 while the Marginal Benefit is $24,000.)

Now lets assume that under the Village police department two things change. Your taxes go up to $200 a year while the added protection decreases the risk of robbery to 0.1% (0.001). This lowers the expected cost of the robbery to $100 dollars. Obviously you would support it over no police force, but would you support it over the next best alternative (the Nassau Police Force.)

Well,

The expected cost of the crime under the Nassau Police force is $1000

The expected cost of the crime uncer the Mineola Police Force is $100

The marginal benefit is therefore $900

On the cost side,

The cost of the Nassau Police force is $100

The cost of the Mineole Police force is $200

The marginal cost is $100

So you should still support it since (MB = $900 which is greater than MC = $100.)

Although these figures do not support or oppose a police force--since I made them up in my head--they do clear away a lot of nonsense such as

1) You should automatically oppose a police force if your tax dollars go up. Not true. If your taxes go up but the benefits go up by MORE then you should still support it. (Note: The Village Mayor believes that the tax change will be neglible. So this point could be moot. But it may not be, so it is worth discussing).

2) How much of a benefit does a community police force bring via increased accountability to the voters and more direct policing? This is hard to estimate (although I could probably do a study if the Village paid me some money and gave me the data---hint hint). But one quick way to estimate is to look at the current villages who do have their own Police Force and then see if they have succeeded or whether they are happy or not. (A quick pass suggests that they are succeeding and are happy, but I stand ready to be refuted by better estimates).

Then you can decide.

The Village of Mineola is considering opting out of the Nassau County Police Force and establishing its own police force (ala Garden City). To read a summary of the debate (scheduled for a vote on Dec 5th), click here. For a more detailed summary, click here

This is certainly a contentious issue, but how can we use economics to wade through the debate?

1) Rational Ignorance and vested interests - The first topic we can use is the idea of government failure. That is, most of the voters are rationally ignorant about how their taxes are being used. How many people here know how much of their property taxes went towards funding the Nassau County Police Department? On the other hand, the Police department has a strong vested interest in maintaining the revenue source coming from Mineola (estimated at $6.7mn dollars a year). Part of the problem seems to be that taxes have gone up while coverage has gone down. A first pass look at this suggests that the increase salaries of police officers over the years has made it harder to hire police officers (since that increases revenues and necessitates a tax hike. With taxes at already high levels in the county, this is a problem.)

On the other hand, the village certainly has a vested interest in making sure the report favors establishing a police department rather than maintaining the current service (although the Village debate mentioned this, they curiously understated the vested interest mentioned above). However, from the standpoint of the Village residents, a Village police force would bring the police closer to the "check" of the voters. That is, if the residents are unsatisfied with how things are going they can vote in a change. The mayor, in turn, has a vested interest in getting re-elected so he is unlikely to want things to spiral out of control. As far as I can tell, the voters do not have this choice under the current police force (since their votes are dispersed among the county).

2) Marginal Utility - However, the economics of government can only take us so far here. The key issue is whether the marginal utility per tax dollar goes up or go down. So the question for residents becomes, how much "juice" (police coverage) am I getting for the "squeeze" (tax dollars). But this makes the whole debate about a tax hike completely irrelevant. If the marginal utility of the tax dollars goes up, you should support it. If it goes down, you should oppose it. Here is how I can demonstrate this:

Assume that initially you pay $100 a year in taxes to the government for police protection (your coverage is the Nassau Police Force). Assume also that there is only one type of crime, robbery, and that crime, if committed, will cost you $100,000. Finally assume that the police force, via the deterrant of arrest and prosecution, lowers the risk of arrest to 1% (0.01). Without a police force the probability of your home being robbed is 25%

The benefit to you of the police force is, of course, huge. Without it the expected cost of a robbery is $25,000. With a police force it is $1000. (According to Marginal Utility theory you should support a measure so long as the MB>MC. Here the Marginal Cost is $200 while the Marginal Benefit is $24,000.)

Now lets assume that under the Village police department two things change. Your taxes go up to $200 a year while the added protection decreases the risk of robbery to 0.1% (0.001). This lowers the expected cost of the robbery to $100 dollars. Obviously you would support it over no police force, but would you support it over the next best alternative (the Nassau Police Force.)

Well,

The expected cost of the crime under the Nassau Police force is $1000

The expected cost of the crime uncer the Mineola Police Force is $100

The marginal benefit is therefore $900

On the cost side,

The cost of the Nassau Police force is $100

The cost of the Mineole Police force is $200

The marginal cost is $100

So you should still support it since (MB = $900 which is greater than MC = $100.)

Although these figures do not support or oppose a police force--since I made them up in my head--they do clear away a lot of nonsense such as

1) You should automatically oppose a police force if your tax dollars go up. Not true. If your taxes go up but the benefits go up by MORE then you should still support it. (Note: The Village Mayor believes that the tax change will be neglible. So this point could be moot. But it may not be, so it is worth discussing).

2) How much of a benefit does a community police force bring via increased accountability to the voters and more direct policing? This is hard to estimate (although I could probably do a study if the Village paid me some money and gave me the data---hint hint). But one quick way to estimate is to look at the current villages who do have their own Police Force and then see if they have succeeded or whether they are happy or not. (A quick pass suggests that they are succeeding and are happy, but I stand ready to be refuted by better estimates).

Then you can decide.

Monday, November 27, 2006

Debate over at Harvard Professor Blog

Harvard Economist Greg Mankiw has linked to the latest Salvo in the ongoing Jeffrey Sachs/Bill Easterly debate (Sachs is a big proponent of foreign aid, Easterly is a noted skeptic).

Sachs latest response offers up the Nordic Economic Models as enviable models for developing (and I guess by implication Developed?) countries to follow. I am not so sure for reasons you can read about here.

This is what most worries me:

But Sweden retained the world´s highest taxes, generous social security systems and a heavily regulated labor market, which split the economy: Sweden is very good at producing goods, but not at producing jobs. According to a recent study of 35 developed countries, only two had jobless growth: Sweden and Finland. Economic growth in Sweden in the last 25 years has had no correlation at all with labor-market participation. (In contrast, 1 percent of growth increases the number of jobs by 0.25 percent in Denmark, 0.5 percent in the United States and 0.6 percent in Spain.) Amazingly, not a single net job has been created in the private sector in Sweden since 1950.

You can read about that here

Sachs latest response offers up the Nordic Economic Models as enviable models for developing (and I guess by implication Developed?) countries to follow. I am not so sure for reasons you can read about here.

This is what most worries me:

But Sweden retained the world´s highest taxes, generous social security systems and a heavily regulated labor market, which split the economy: Sweden is very good at producing goods, but not at producing jobs. According to a recent study of 35 developed countries, only two had jobless growth: Sweden and Finland. Economic growth in Sweden in the last 25 years has had no correlation at all with labor-market participation. (In contrast, 1 percent of growth increases the number of jobs by 0.25 percent in Denmark, 0.5 percent in the United States and 0.6 percent in Spain.) Amazingly, not a single net job has been created in the private sector in Sweden since 1950.

You can read about that here

The Economics of Now

This is an interesting article on why people seem to consume too much now, rather than later.

GAP is struggling

This WSJ article is about the ongoing struggles of the clothing company Gap. Although a company like the Gap is best modeled using "monopolistic competition," even that type of industry is subject to competitive pressures:

"None of these projects addresses the once highflying retailer's major problem: how to revive sales broadly at the uncompetitive Gap and Old Navy divisions. The enormous chains, with 1,338 and 1,008 stores, respectively, in the U.S. and Canada, need to appeal to broad audiences, which has made them vulnerable to growing competition. Gap's classic styles have been widely copied, and it now competes with everything from department stores to teen-focused specialty retailers such as American Eagle Outfitters Inc. Old Navy has failed to stay ahead of discount competitors whose fashion sense is growing"

One way for a company like the Gap to continue to earn economic profits is through constant remodelling of its brand (new sweaters and jeans) and advertising (the whole Red line thing). But lets be honest, how good are the new Gap sweaters? Anyone? And how many Polo shirts can one buy before enough is enough?

"None of these projects addresses the once highflying retailer's major problem: how to revive sales broadly at the uncompetitive Gap and Old Navy divisions. The enormous chains, with 1,338 and 1,008 stores, respectively, in the U.S. and Canada, need to appeal to broad audiences, which has made them vulnerable to growing competition. Gap's classic styles have been widely copied, and it now competes with everything from department stores to teen-focused specialty retailers such as American Eagle Outfitters Inc. Old Navy has failed to stay ahead of discount competitors whose fashion sense is growing"

One way for a company like the Gap to continue to earn economic profits is through constant remodelling of its brand (new sweaters and jeans) and advertising (the whole Red line thing). But lets be honest, how good are the new Gap sweaters? Anyone? And how many Polo shirts can one buy before enough is enough?

Friday, November 24, 2006

Movie Ticket Pricing

Here is another explanation for why theatres do not charge variable pricing for movies (i.e. a higher ticket price for Spiderman and a lower price for Gigli). The answer, according to some research, is market power on the part of the distribution companies.

Thursday, November 23, 2006

Test Averages

I was more satisfied with Test 2 than I was with Test 1

Overall the average was 76.5 with a median of 78 (meaning the class tilted slightly towards the higher end.

Compared to test one the average was 73.8 with a median of 75.

There were less low grades than there was last time, rather than more high grades among people who did well on Test 1. That accounts for the increase.

Happy Thanksgiving.

Overall the average was 76.5 with a median of 78 (meaning the class tilted slightly towards the higher end.

Compared to test one the average was 73.8 with a median of 75.

There were less low grades than there was last time, rather than more high grades among people who did well on Test 1. That accounts for the increase.

Happy Thanksgiving.

Wednesday, November 22, 2006

Monday, November 20, 2006

Quiz 8 - Question 10 explanation

#10 is the question that most people got wrong. (Answer D), with C being the main answer people who got it wrong gave.

A and B do not make sense for a natural monopoly so the question is whether C or D is the better answer. C asks you whether a company that owns a large portion of a countries natural resources could be considered a natural monopolist. D asks you whether an industry with extensive economies of scale could be considered a natural monopolist.

C cannot be a natural monopolist because a natural monopoly is both inevitable and desirable. That is, it is not inevitable that a Diamond Company controls all the worlds diamonds and then exists as a natural monopoly. The same with Wheat, grain, or oil. You don't have to have one company running the business, it just ended up occuring. The government can step in and break up this company without undo social harm.

This is not the case with D because the large economies of scale mean that any breakup of the company raises ATC (remember the graph). Higher costs mean higher prices. Higher prices lead to less quantity demanded (remember the demand curve). So breaking up the monopolist is undesirable. In other words, if you get your electricity from LIPA or Con Edison, you do not want that company broken up because smaller companies cannot offer you electricity as cheaply as the one company you currently have.

A and B do not make sense for a natural monopoly so the question is whether C or D is the better answer. C asks you whether a company that owns a large portion of a countries natural resources could be considered a natural monopolist. D asks you whether an industry with extensive economies of scale could be considered a natural monopolist.

C cannot be a natural monopolist because a natural monopoly is both inevitable and desirable. That is, it is not inevitable that a Diamond Company controls all the worlds diamonds and then exists as a natural monopoly. The same with Wheat, grain, or oil. You don't have to have one company running the business, it just ended up occuring. The government can step in and break up this company without undo social harm.

This is not the case with D because the large economies of scale mean that any breakup of the company raises ATC (remember the graph). Higher costs mean higher prices. Higher prices lead to less quantity demanded (remember the demand curve). So breaking up the monopolist is undesirable. In other words, if you get your electricity from LIPA or Con Edison, you do not want that company broken up because smaller companies cannot offer you electricity as cheaply as the one company you currently have.

Saturday, November 18, 2006

Answers to Quiz 8

I will try and post explanations for questions that were answered wrong by a majority of the class.

1) D

2) B

3) C

4) C

5) D

6) B

7) B

8) D

9) A

10) D)

1) D

2) B

3) C

4) C

5) D

6) B

7) B

8) D

9) A

10) D)

Thursday, November 16, 2006

Milton Friedman

Milton Friedman was one of the greatest economists of the 20th century. He just passed away today at the age of 94. Most of you might not know who he is but both this class and, to a greater extent, the macro class you will take are heavily influenced by his thought (even if the professor does not mention his name.

The New York Times has an good obituary here.

Here are some other reactions.

The is a great summary of his beliefs:

"Outside monetary affairs Friedman remained a mainstream economist. As he himself wrote in Capitalism and Freedom (a book published in 1962 which meant went much deeper than Free to Choose) he could offer no hard and fast line for the limits of government intervention. But he believed that an objective study of the facts, case by case, combined with an underlying belief in personal choice, would usually swing the argument in favour of private provision in the market place"

The New York Times has an good obituary here.

Here are some other reactions.

The is a great summary of his beliefs:

"Outside monetary affairs Friedman remained a mainstream economist. As he himself wrote in Capitalism and Freedom (a book published in 1962 which meant went much deeper than Free to Choose) he could offer no hard and fast line for the limits of government intervention. But he believed that an objective study of the facts, case by case, combined with an underlying belief in personal choice, would usually swing the argument in favour of private provision in the market place"

Wednesday, November 15, 2006

Reminder

There is an in class quiz this class Thurs Nov 17th.

If you skip out on this class then you miss the in class quiz and hence will be penalized, unless you contact me before the class with a valid excuse.

If you skip out on this class then you miss the in class quiz and hence will be penalized, unless you contact me before the class with a valid excuse.

Good posts on Healthcare

Read this here for the difficulties facing US Health Care. The moral of the story is that it will not be easy to slow down growth in medical spending, nevermind cut medical spending.

You may also be interested in this essay on how to reform the US Welfare State. The author's plan is an attempt to harness competition in the presence of market failure. In the case the health care market is riddles with information problems, specifically adverse selection and moral hazard. His proposal resembles the voucher system I was discussing in class last night.

You may also be interested in this essay on how to reform the US Welfare State. The author's plan is an attempt to harness competition in the presence of market failure. In the case the health care market is riddles with information problems, specifically adverse selection and moral hazard. His proposal resembles the voucher system I was discussing in class last night.

How Rich are you

If you think you are poor or rich you can test to see where you rank compared with the rest of the world here.

Drug prices and R&D

As we discussed last night, one possible negative side effect of negotiating lower drug prices due to large market power is a decrease in research and development in new drugs. This post--and paper--provides evidence of this. It's worth a look.

Tuesday, November 14, 2006

So you don't learn about externalities or monopoly?

This is an interesting post on how students in an intro Economics class did not learn about market imperfections such as externalities, monopolistic competition or the trade off between efficiency and equity. A good response can be read here (scroll to the second point).

Here is an interesting assignment for you that can count towards extra credit. Name and explain the various market imperfections and qualifications we discussed in this class.

Here is an interesting assignment for you that can count towards extra credit. Name and explain the various market imperfections and qualifications we discussed in this class.

Economist post on European vs American Growth

Here is an interesting post on European Growth vs American Growth

The key thing here is that Europe has higher taxes and more generous benefits, which tend to slow growth. You can use your economics training to explain how this might be the case.

The big debate is whether it is worth it or not. On the one hand, it slows growth so their economies do not grow as fast as the US. On the other hand, the benefits do yield gains for citizens right now (in the form of higher unemployment benefits, more vacations, etc.) The counter-argument is: sure it works fine now, but in 50 years this means that the income disparity and growth in the US will be much, MUCH more than it is now. How appealing will be the current model then?

The key thing here is that Europe has higher taxes and more generous benefits, which tend to slow growth. You can use your economics training to explain how this might be the case.

The big debate is whether it is worth it or not. On the one hand, it slows growth so their economies do not grow as fast as the US. On the other hand, the benefits do yield gains for citizens right now (in the form of higher unemployment benefits, more vacations, etc.) The counter-argument is: sure it works fine now, but in 50 years this means that the income disparity and growth in the US will be much, MUCH more than it is now. How appealing will be the current model then?

Friday, November 10, 2006

Quiz 7 (Due in Class Tues Nov 14th)

{kind=link}

Quiz 7 – Perfect Competition (Due in Class Tuesday 14th)

Professor Matthew Festa

1) State the 4 assumption of Perfect Competition and explain the meaning behind them (2 points)

2) In the graph below, what will happen if the producer produces more? What will happen if he produces less? Why is this the case? (2 points).

3) In the graph below, why is the market out of equilibrium? What will happen to price and output as competition corrects the imperfection in the market (2 points).

4)In the graph below, why does the monopolist enjoy economic (or monopoly profits? Why can’t the market compete these extra profits away? (2 points).

5) If the authorities attempt to force the monopolist to produce at P = MC, what is the problem from the standpoint of profits?. Base your answer on the graph of the monopolist? (2 points).

Upcoming events before Thanksgiving

I am very sorry I had to cancel class last night, but I got sick with an eye infection and had to see the doctor. Unfortunately, that meant I could not give you the outline for the next few weeks, so let me do that now.

1) The next quiz (Quiz 7) will be due on Tuesday. I am working on it now and it should be up today.

2) I am planning on an 8th quiz, in class, on Tuesday as well. It will be 10 quick multiple choice questions, each worth 1 point each. I am doing this to give you a base to see what type of questions will be on Test 2.

3) Test 2 will be Tues 21st. So I got it in before Thanksgiving.

If you have any further questions please feel free to e-mail me.

1) The next quiz (Quiz 7) will be due on Tuesday. I am working on it now and it should be up today.

2) I am planning on an 8th quiz, in class, on Tuesday as well. It will be 10 quick multiple choice questions, each worth 1 point each. I am doing this to give you a base to see what type of questions will be on Test 2.

3) Test 2 will be Tues 21st. So I got it in before Thanksgiving.

If you have any further questions please feel free to e-mail me.

Tuesday, November 07, 2006

Walmart and Marginal Cost

This post at Econlog explains how Walmart has bid down extra profits (that is MB>MC) due to their large size. Since Walmart can switch suppliers, the supplier will lower his price and thus MB comes closer to Marginal Cost.

The main effect is to lower prices, especially for the poor.

The main effect is to lower prices, especially for the poor.

Saturday, November 04, 2006

2006 Mid-Term Elections and Perfect Competition

One way to examine how competition works in the economy is to look at the Stock Market. An interesting market that has popped up in recent years has been the prediction markets such as tradesports. Tradesports has been a good predictor of previous elections, books, popes and other events.

For this year, tradesports has a prediction market up for "Republican controll of congress during the midterm election." You can view their current up to date predictions here.

The market is currently predicting the Democrats to take over the House of Representatives (by a large portion) and the Republicans to hold on to the Senate (although if you look at the predictions for each individual race, the market is predicting a large Democratic pickup).

The main reason why these markets have been so good at predicting events is that there are a lot of people trying to make money of these things. Since they have to put their money where their mouth is, they overall bet they make tends to be very accurate. If someone tries to screw up the market, then other people re-enter with money and bid back the contract to its equilibrium price.

Let's see how accurate this prediction is on Tuesday.

For this year, tradesports has a prediction market up for "Republican controll of congress during the midterm election." You can view their current up to date predictions here.

The market is currently predicting the Democrats to take over the House of Representatives (by a large portion) and the Republicans to hold on to the Senate (although if you look at the predictions for each individual race, the market is predicting a large Democratic pickup).

The main reason why these markets have been so good at predicting events is that there are a lot of people trying to make money of these things. Since they have to put their money where their mouth is, they overall bet they make tends to be very accurate. If someone tries to screw up the market, then other people re-enter with money and bid back the contract to its equilibrium price.

Let's see how accurate this prediction is on Tuesday.

Friday, November 03, 2006

Quiz 6 due Nov 7

Quiz 6 – Production Theory

Professor Matthew Festa

Due in Class: Tuesday Nov 7th

1) (2points) Jim quits his job as a construction worker to open his own construction business. Jim’s revenues are $150,000 while the costs of operating are $100,000 (included in this number is $10,000 in order to purchase equipment, an office and other expenses in order to open the business). The salary at his old job was $40,000 a year. In order to obtain the $10,000 to open his business he took out his savings of $10000, which earned him $1,000 a year in income.

a. What is his accounting profit?

b. What is his economic profit?

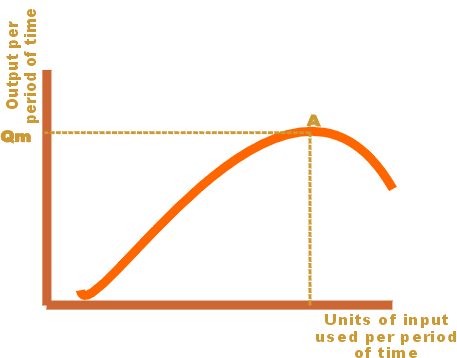

2) Based on the following 2 graphs, tell me where productivity per worker is increasing at an accerating rate, where it is increasing at a diminishing rate and where it starts declining. Why does total production begin to decline after point a? (use the textbook as a reference). (2 points).

3) Calculate the ATC and the Marginal Total Cost for the following. (4 points).

Q TVC TFC

0) 0 100

1) 10 100

2 )15 100

3) 18 100

4) 23 100

5) 33 100

6) 45 100

4) How much can be produced while costs are decreasing (2 points).

Professor Matthew Festa

Due in Class: Tuesday Nov 7th

1) (2points) Jim quits his job as a construction worker to open his own construction business. Jim’s revenues are $150,000 while the costs of operating are $100,000 (included in this number is $10,000 in order to purchase equipment, an office and other expenses in order to open the business). The salary at his old job was $40,000 a year. In order to obtain the $10,000 to open his business he took out his savings of $10000, which earned him $1,000 a year in income.

a. What is his accounting profit?

b. What is his economic profit?

2) Based on the following 2 graphs, tell me where productivity per worker is increasing at an accerating rate, where it is increasing at a diminishing rate and where it starts declining. Why does total production begin to decline after point a? (use the textbook as a reference). (2 points).

3) Calculate the ATC and the Marginal Total Cost for the following. (4 points).

Q TVC TFC

0) 0 100

1) 10 100

2 )15 100

3) 18 100

4) 23 100

5) 33 100

6) 45 100

4) How much can be produced while costs are decreasing (2 points).

Thursday, November 02, 2006

Perfect Competition

This article in Wikipedia explains in 2 pages what it takes the book 20 pages to do. If I were you, I would print this article out

Note: Do you see the importance of mastering the basics of Chapter 9 (production theory)?

Also this graph is the jist of the theory.

Note: Do you see the importance of mastering the basics of Chapter 9 (production theory)?

Also this graph is the jist of the theory.

Facebook and Pigouvian Taxes

If you are a member of facebook you want to join the Pigou club, click here.

Note: Remember that the Pigouvian taxes are one way to rectify a market imperfection, which according to our Physic's professor friend, we don't really talk about enough....

Note: Remember that the Pigouvian taxes are one way to rectify a market imperfection, which according to our Physic's professor friend, we don't really talk about enough....

Physics professor Criticizes Economics

This here is an article and discussion that would make an excellent extra credit project.

Quick Question: How long did it take for me to raise complications/caveats/problems/limits in basic supply and demand theory?

Further, I take issue with the suggestion that economists are not concerned with irrational behavior. It's all over the literature right now and the problem seems to be somewhat overblown (despite bubbles, the market is curiously efficient in my opinion).

Quick Question: How long did it take for me to raise complications/caveats/problems/limits in basic supply and demand theory?

Further, I take issue with the suggestion that economists are not concerned with irrational behavior. It's all over the literature right now and the problem seems to be somewhat overblown (despite bubbles, the market is curiously efficient in my opinion).

Thursday, October 26, 2006

Quiz 5 due Tuesday Oct 31st

Quiz 5 – Consumer Theory

Professor Matthew Festa

Due in Class Tuesday Oct 31st

1) State the law of diminishing marginal utility. Reproduce the Total Utility Graph and Marginal Utility graph from the chapter and explain why Total Utility begins to decline after the 6th unit consumed (2 points).

2) State and explain all 4 theories of consumer behavior (1 points).

3) The marginal benefit Joe gains from going to watch the Mets is $200 dollars while the marginal Utility he gets from going to the Movies is $80 dollars. A met game costs $100 dollars (this is the playoffs) while the movie of the week, which his girlfriend wants to see, costs $10. Given a choose between the 2,which one would he choose that night? (2 points).

4) Consumer theory states that consumers will always manage their consumption so that the marginal benefit of one product equals the marginal benefit of another product. Explain why this is the case.

For reference, explain why MU/$ of A = MU/$ of B (1 points).

5) Joan has $14 in income and she can spend the money on either pizza or ice cream. The price of pizza is $2 dollars and the price of ice cream is 1$. What combination of pizza and ice cream will she purchase given the following MB (which are not converted into MB per dollar terms!!!)

Pizza

1) 24

2) 20

3) 18

4) 16

5) 12

6) 6

7) 4

Ice cream

1) 10

2) 8

3) 7

4) 6

5) 5

6) 4

7) 3

Professor Matthew Festa

Due in Class Tuesday Oct 31st

1) State the law of diminishing marginal utility. Reproduce the Total Utility Graph and Marginal Utility graph from the chapter and explain why Total Utility begins to decline after the 6th unit consumed (2 points).

2) State and explain all 4 theories of consumer behavior (1 points).

3) The marginal benefit Joe gains from going to watch the Mets is $200 dollars while the marginal Utility he gets from going to the Movies is $80 dollars. A met game costs $100 dollars (this is the playoffs) while the movie of the week, which his girlfriend wants to see, costs $10. Given a choose between the 2,which one would he choose that night? (2 points).

4) Consumer theory states that consumers will always manage their consumption so that the marginal benefit of one product equals the marginal benefit of another product. Explain why this is the case.

For reference, explain why MU/$ of A = MU/$ of B (1 points).